Mike Chen, a licensed Florida real estate broker and STR manager at FunStay Florida, has walked hundreds of Orlando homeowners through the insurance question. The answer is rarely simple. Short-term rental insurance in Orlando is not a single policy. It is a stack of coverage types that work together to protect the property, the revenue, and the owner from liability. Getting it wrong is one of the most expensive mistakes in the vacation rental business.

Florida classifies vacation rentals as public lodging under Chapter 509 of the Florida Statutes. That classification makes every Orlando STR a commercial operation in the eyes of the state, subject to the same rental laws as hotels. Standard homeowner’s insurance was never built for that, and most policies exclude it entirely.

Short-term rental insurance in Orlando typically requires six coverage types: a DP-3 dwelling policy, general liability, loss of rents, contents protection, a separate flood policy, and a commercial umbrella. The full stack costs roughly $3,100 to $7,200 per year for a 4-5 bedroom vacation home in the Disney corridor.

Here is what each coverage type does, what it costs, and where the gaps hide.

Why Your Homeowner’s Policy Will Not Cover Your STR

A standard HO-3 homeowner’s policy is designed for owner-occupied or long-term tenant use. The moment a property starts accepting nightly guests through Airbnb, VRBO, or direct bookings, it shifts into commercial territory. That shift triggers exclusions in nearly every standard policy.

The most common failure happens like this: an owner buys a home in one of the top resort communities, insures it on a regular homeowner’s policy, then lists it on Airbnb. Everything works fine until a guest slips by the pool or a kitchen fire causes damage. The carrier investigates, discovers the property was operating as a short-term rental, and denies the claim for undisclosed commercial use.

⚠️The most expensive coverage gap we see:

Undisclosed commercial use on a personal-lines policy. The claim gets denied, the policy gets cancelled, and the owner faces both the repair cost and the lost revenue with no coverage. This pattern accounts for most “my insurance did not pay” stories from Florida hosts.

Orlando STR owners need a DP-3 dwelling policy (for single-family homes) or an HO-6 policy (for condos) that explicitly permits short-term rental use. These forms are built for commercial occupancy and priced accordingly.

Six Coverage Types Every Orlando STR Owner Needs

Short-term rental insurance in Orlando is not one policy. It is a program built from several coverage lines, each protecting against a different risk. Here is what a complete stack looks like for a typical 4-5 bedroom vacation home near Disney.

| Coverage | What It Protects | Annual Cost |

|---|---|---|

| Dwelling (DP-3) | Structure, roof, systems. Written for commercial occupancy with named-storm wind deductible. | Included in program |

| General Liability | Guest injuries, slip-and-falls, pool accidents. $1M per occurrence / $2M aggregate recommended. | Included in program |

| Loss of Rents | Replaces booking revenue when a covered loss makes the property unrentable. Critical during peak season. | Included in program |

| Contents & Furnishings | Furniture, electronics, appliances, linens. Covers guest-caused damage and theft. | Included in program |

| Flood Insurance | Excluded from every property policy. Separate NFIP or private flood policy required. | $700 – $2,000+ |

| Umbrella / Excess | Adds $1M+ above primary liability. Must be commercial, not personal umbrella. | $400 – $1,200 |

The first four coverages are typically bundled into a single STR program. For an inland Orlando property, that full program runs roughly $2,000 to $4,000 per year. Flood and umbrella sit on top as separate policies, bringing the total to approximately $3,100 to $7,200 per year depending on property value and coverage limits.

💡 Named-storm wind deductible:

Florida STR policies carry a separate hurricane deductible that is a percentage of dwelling value, not a flat dollar amount. On a $500,000 home, a 5% wind deductible means $25,000 out of pocket before the policy responds to hurricane damage. This number does not show up in the annual premium but is one of the most important figures on a Florida STR policy.

Insurance is a significant line item in overall operating costs. It typically runs 3% to 6% of gross rental revenue for a well-managed Orlando property. Working with experienced management services helps owners build the right short-term rental insurance stack from day one.

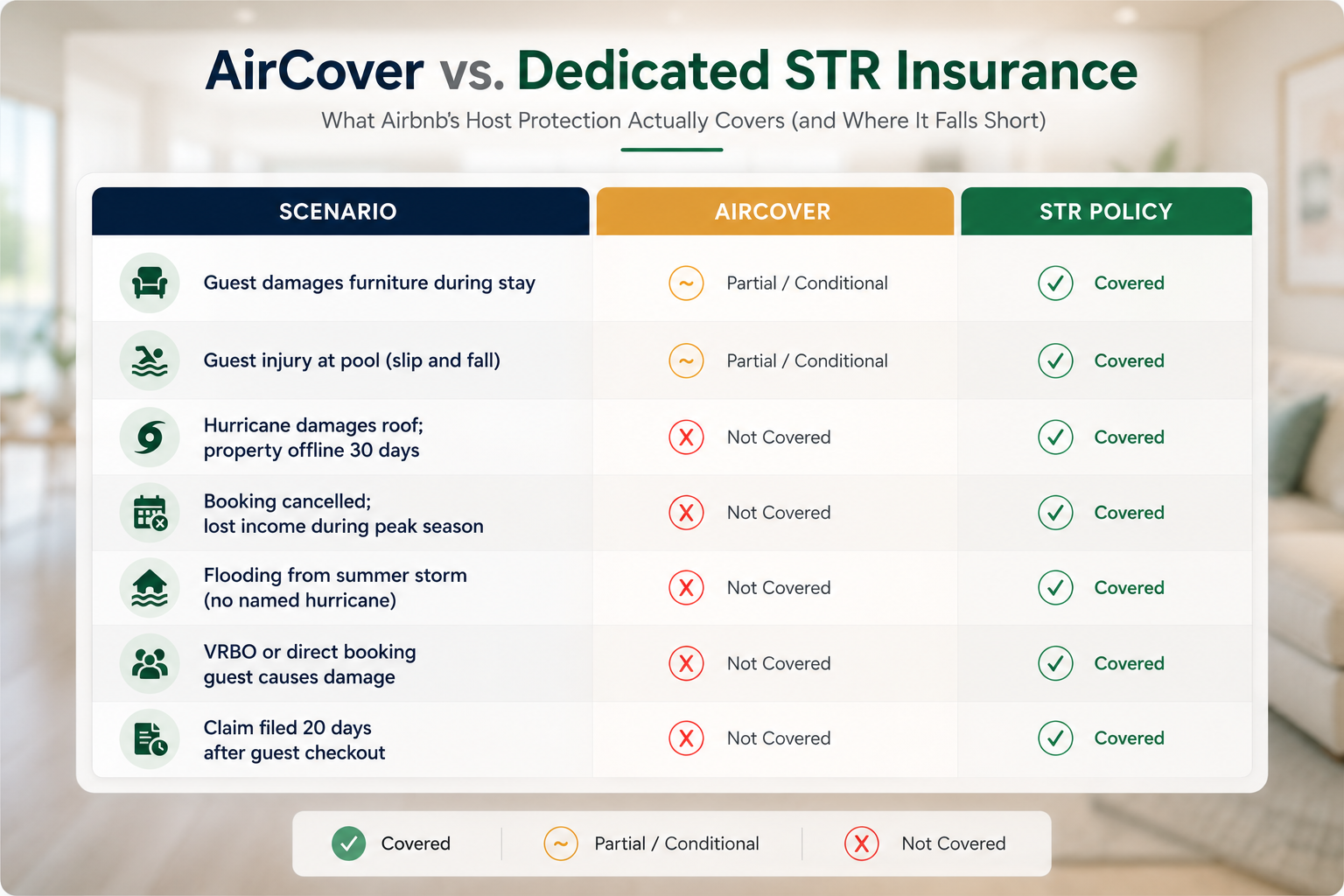

What Airbnb AirCover Actually Covers (and What It Does Not)

AirCover provides up to $3 million in host damage protection and $1 million in liability coverage. Those numbers look reassuring on the surface, but AirCover is a reimbursement program with significant exclusions. It is not an insurance policy.

| Scenario | AirCover | STR Policy |

|---|---|---|

| Guest breaks furniture | ✓ Covered (14-day filing) | ✓ Covered |

| Guest injured at pool | ✓ Limited liability | ✓ Full commercial GL |

| Hurricane damages roof | ✗ Not covered | ✓ Covered (wind deductible) |

| Lost bookings during repairs | ✗ Not covered | ✓ Loss of rents |

| VRBO or direct bookings | ✗ Airbnb only | ✓ All platforms |

| Damage between guests | ✗ Booking period only | ✓ 24/7 coverage |

| Flood damage | ✗ Not covered | ✗ Separate flood policy |

| Theft of cash or jewelry | ✗ Not covered | Varies by policy |

As of March 2025, Airbnb made AirCover secondary for hosts managing six or more listings. That means a host’s own insurance must respond first before AirCover pays anything. VRBO does not offer host insurance at all, making a dedicated STR policy essential for owners listing on multiple platforms.

AirCover claims also require documentation within 14 days of guest checkout (or before the next guest checks in, whichever comes first), including timestamped photos and professional repair quotes. Missing that window means the claim is denied regardless of the damage. In April 2026, Airbnb also introduced a “reasonable care” standard that reduces payouts for repeat claims or properties with insufficient maintenance.

For owners focused on maximizing bookings alongside proper coverage, strong listing optimization and the right short-term rental insurance in Orlando work together to protect both revenue and the property itself.

Pool Liability and Florida’s Safety Requirements

Nearly every Orlando vacation rental has a pool, and pool areas generate the highest liability exposure of any amenity. Beyond the standard Airbnb essentials that every property needs, pool safety requires its own layer of protection. Florida’s Residential Swimming Pool Safety Act requires at least one approved safety feature on every vacation rental pool. The options include a four-foot barrier fence with self-latching gate, a power safety cover, door exit alarms with a minimum 85 dB rating, or an approved pool alarm meeting ASTM Standard F2208.

A July 2026 update to the law makes vacation rental operators directly liable for actual damages if the required safety features are not in place. That liability exists regardless of insurance, but carrying proper coverage ensures a financial backstop if a pool incident does occur.

For pool homes, the standard recommendation is $1 million in general liability paired with a $1 million commercial umbrella. The umbrella costs roughly $400 to $1,200 per year and is one of the most cost-efficient coverages in the entire program. Standard personal umbrella policies typically exclude business activities, so the umbrella must be structured as commercial or carry an STR endorsement.

💡 Screen enclosure note:

Pool cage rescreening in Central Florida runs $1,500 to $4,500, and full enclosure replacement after storm damage can run $12,000 to $20,000 or more depending on size. Tropical storms and hurricanes can destroy screen enclosures that survive years of normal weather. Make sure the dwelling policy covers detached structures and screen enclosures specifically.

How to Choose the Right STR Insurance Provider

Not every insurance carrier writes short-term rental policies, and not every agent understands the Orlando vacation rental market. Here is what to look for when shopping for short-term rental insurance in Orlando.

First, confirm the carrier explicitly writes STR coverage. A landlord endorsement on a standard policy is not the same thing. The policy form should be a DP-3 or commercial habitational form that names transient occupancy as a covered use.

Second, check the flood insurance situation separately. Flood is always a different policy, and most Orlando resort communities in Osceola and Polk counties sit outside FEMA high-risk zones. That does not mean flood risk is zero. Summer storms and tropical weather still produce inland flooding. Budget for flood as a standalone line item.

Third, ask about the named-storm wind deductible before comparing premiums. A lower annual premium often means a higher wind deductible. On a $500,000 home, the difference between a 2% and 5% deductible is $15,000 in out-of-pocket exposure per hurricane claim.

Fourth, verify the policy includes loss of rents coverage. A property shut down for repairs during holiday season can lose $8,000 to $15,000 in bookings. Without loss of rents coverage, that income simply disappears.

Several carriers specialize in Florida STR coverage. When evaluating quotes, focus on the coverage structure and deductibles rather than the premium alone. The cheapest short-term rental insurance in Orlando is the one that actually pays when something goes wrong. Pair the right coverage with strong property styling and guest screening to reduce claims in the first place.

{kind=link}