AirCover promises $3 million in free protection. It won’t cover hurricanes, pool accidents, or your VRBO bookings.

AirCover is free, automatic, and the numbers look great: $3 million in damage protection, $1 million in liability.

Then a guest trashes your pool deck. A storm rips off the lanai. Someone slips on a wet tile, and their lawyer calls. That’s when the Airbnb AirCover vs insurance question stops being theoretical.

If you own a vacation rental in Orlando, Kissimmee, or Davenport, the fine print hits harder than anywhere else. Florida has hurricanes, pool liability, strict premises liability laws, and counties that now require proof of Airbnb host insurance that Florida operators can actually rely on.

What AirCover Actually Is (and Isn’t)

So what does AirCover cover? It bundles two very different things under one name.

Host Damage Protection(up to $3 million) covers guest-caused damage, pet damage, deep cleaning, and lost income from cancelled bookings. This is not insurance. Airbnb decides whether to pay, how much, and when. No independent adjuster, no binding arbitration.

Host Liability Insurance (up to $1 million) covers bodily injury and property damage claims. This one is actual insurance, underwritten by Generali U.S. Branch. Primary for hosts with fewer than 6 listings. Excess for 6+ (your insurance pays first).

The $3 million number is not an insurance policy.

It’s a voluntary guarantee. When there’s a dispute, the same company that profits from your bookings decides whether you get paid. That’s the core problem with Airbnb AirCover vs insurance from an actual insurer.

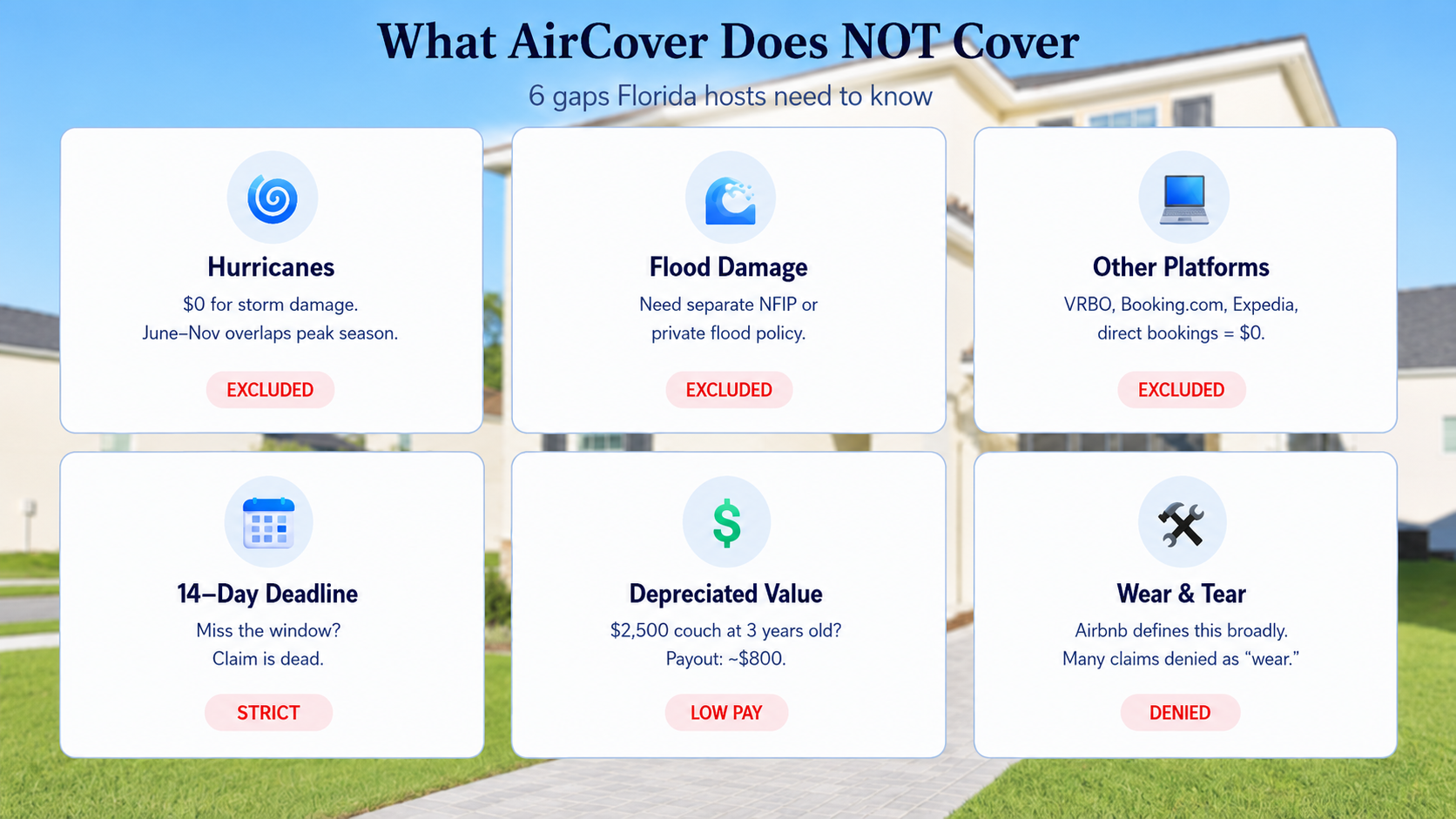

What AirCover Does Not Cover

The AirCover exclusions are significant. Several of them hit Florida hosts harder than anyone.

Hurricanes and natural disasters. $0 for storm damage. Florida’s hurricane season (June through November) overlaps peak rental season.

Flood damage. Not covered. You need a separate NFIP or private flood policy.

Non-Airbnb bookings. VRBO, Booking.com, Expedia, Google Vacation Rentals, direct bookings. Zero AirCover protection.

Claims after 14 days. Report within 14 days of checkout. Full documentation due within 30 days. Miss the AirCover 14-day claim window and the claim is dead.

Depreciated value only. Pays actual cash value, not replacement cost. A $2,500 couch at 3 years old might get $800.

Wear and tear. Airbnb defines this broadly. Stained mattresses, scratched floors, and chipped counters often get classified as wear, not damage.

If 40% of your bookings come from outside Airbnb, 40% of your business is unprotected. The AirCover limitations hit multi-channel hosts the hardest.

What Hosts Actually Get Paid

Hosts report receiving 20 to 50 percent of their claimed amounts after depreciation. The most common reason for an AirCover claim denied is “insufficient documentation,” roughly half of all rejections.

$200,000 in Damage

Cornell Case, 2026

Six students destroyed woodwork, walls, antique rugs, and a family heirloom over 8 days. Airbnb’s investigator called it “standard wear and tear.” The host filed a $540,000 lawsuit.

$80,000 in Biohazard Cleanup

7 Months to Resolve

Full property remediation needed. Seven months of back-and-forth. Final payout: roughly $50,000. The host absorbed the $30,000 gap.

Depreciated value vs. replacement cost is the real difference.

That $2,500 sofa? Airbnb offers $800 after depreciation. Real vacation rental insurance pays what a new equivalent costs. A few hundred dollars per year in premium separates the two. Thousands of dollars separate the payouts.

April 2026 update: Airbnb’s revised Host Damage Protection terms now ban AI-enhanced photos in claims and add a “reasonable care” requirement. More ways to deny. Nothing that raises what you get paid.

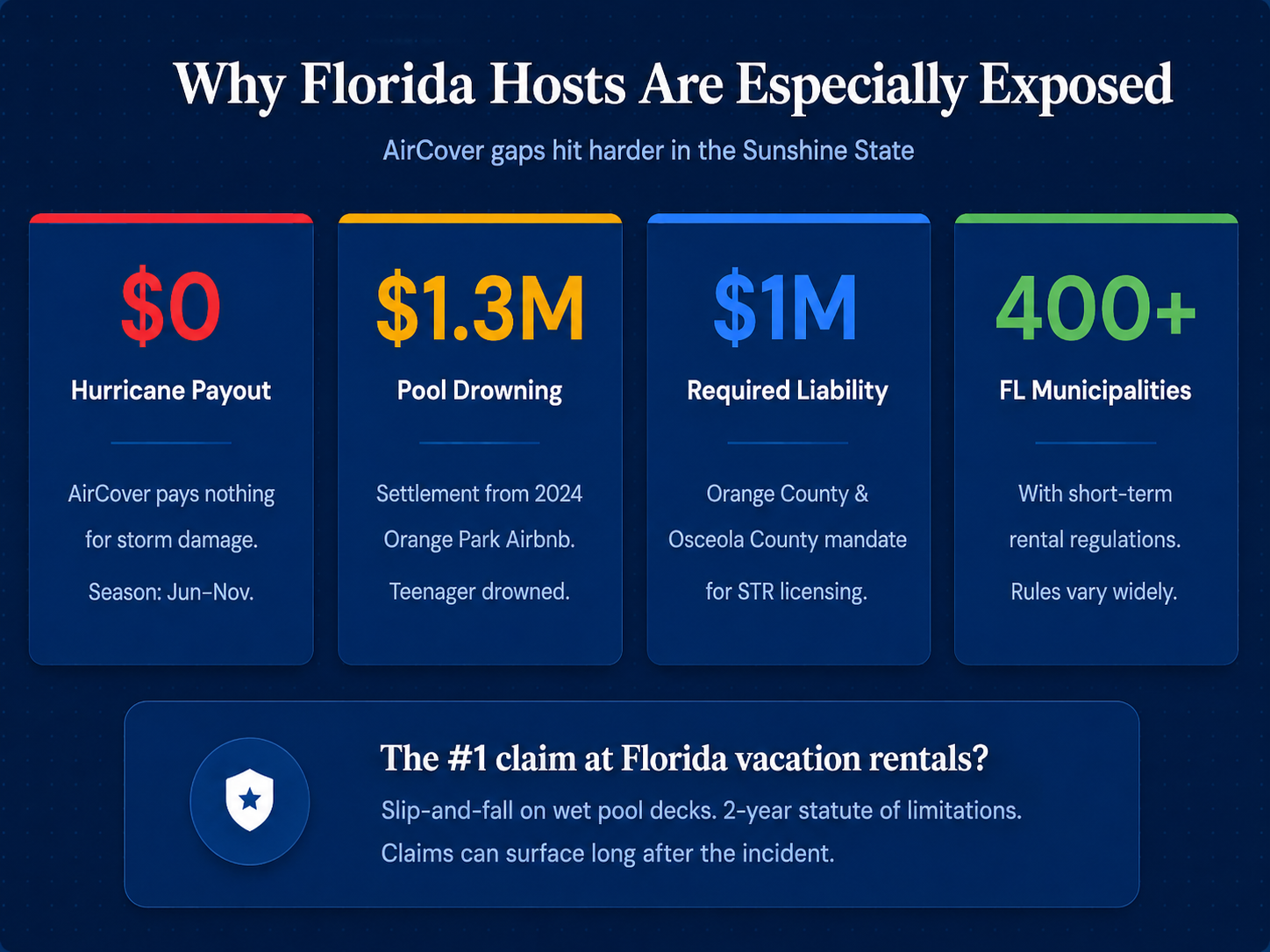

Why Florida Hosts Are Especially Exposed

Most articles about Airbnb AirCover vs insurance treat the topic generically. The risks are not generic if you own a rental in Central Florida.

Hurricane Season Overlaps Peak Rental Season

June 1 through November 30. AirCover excludes natural disasters entirely, so storm damage during a guest stay gets $0.

If your homeowners insurer discovers you’ve been renting undisclosed, they can deny the hurricane claim too. You need a dedicated STR policy with named-storm and wind coverage.

Pool Liability Is Massive

Under Florida law, paying guests are classified as “invitees,” the highest duty of care. You’re responsible for maintaining a safe property and conducting regular inspections.

In 2023, a teenager drowned at an Orange Park Airbnb. The case resulted in a $1.3 million settlement in 2024. Pool safety compliance and proper liability coverage are not optional.

Local Insurance Mandates

Both Orange County and Osceola County require $1 million liability insurance for STR licensing. AirCover alone may not satisfy these requirements depending on your listing count.

Slip-and-Fall: The #1 Claim

Wet pool decks plus Florida humidity create the most common injury scenario at vacation rentals. Statute of limitations is two years, so a claim can surface long after the incident.

Your Homeowners Insurance Won’t Save You Either

Most homeowner policies include a business activity exclusion that denies claims related to vacation rentals. If your insurer discovers you’ve been running an Airbnb without disclosing it, they can deny all claims. Not just guest-related ones.

This is treated as misrepresentation that can void your entire policy. Your insurer can cancel on discovery, putting you in violation of your mortgage agreement.

Florida insurers are actively flagging Airbnb and VRBO listings.

If you’re running a short-term rental on a standard homeowners insurance Airbnb policy without disclosure, you’re operating without real coverage. AirCover supplements proper insurance. It doesn’t replace it.

Airbnb AirCover vs Insurance: Side by Side

| Feature | AirCover | Dedicated STR Insurance |

|---|---|---|

| Cost | Free | $2,000 to $3,000/year in FL |

| Damage limit | $3 million | $300K to $1M+ |

| Liability | $1M (primary or excess*) | $1M+ (primary) |

| Valuation | Depreciated value | Replacement cost |

| Filing deadline | 14 days | 30 to 60 days |

| VRBO / Booking / direct | No | Yes, all platforms |

| Independent adjuster | No | Yes |

| Hurricane / wind | No | Yes |

| Pool liability | Primary or excess* | Primary |

| Loss of income | Limited | Actual loss sustained |

| Legally enforceable | No (ToS) | Yes (contract) |

The core difference: With AirCover, the same company that profits from your bookings decides whether to pay. With real insurance, an independent adjuster evaluates your claim under a binding contract. That’s what Airbnb AirCover vs insurance really comes down to.

Not Sure What Coverage You Need?

We connect our owners with trusted insurance providers and set up damage protection across every booking channel.

What Real Vacation Rental Insurance Covers

A dedicated short-term rental insurance Florida policy covers all your booking channels, uses independent adjusters, and pays replacement cost.

Proper Insurance specializes in STRs across all 50 states. $1M+ liability, pool and amenity coverage, liquor liability, replacement cost, and unlimited business revenue loss. Custom quotes.

Steadily covers all platforms with competitive Florida rates. Straightforward policies, fast-growing since 2020.

CBIZ is strong for pool properties. Up to $2M aggregate liability, built-in income loss protection. Roughly $3/day to $100/month.

Safely offers per-booking insurance at $5 to $12 per reservation. Better fit for lower-volume hosts just starting out.

Don’t skip the umbrella.

For pool properties in Florida, an umbrella policy adding $1M in coverage costs $400 to $1,200/year. One pool accident lawsuit can reach seven figures. That’s the cheapest protection you can buy for your vacation rental pool liability exposure.

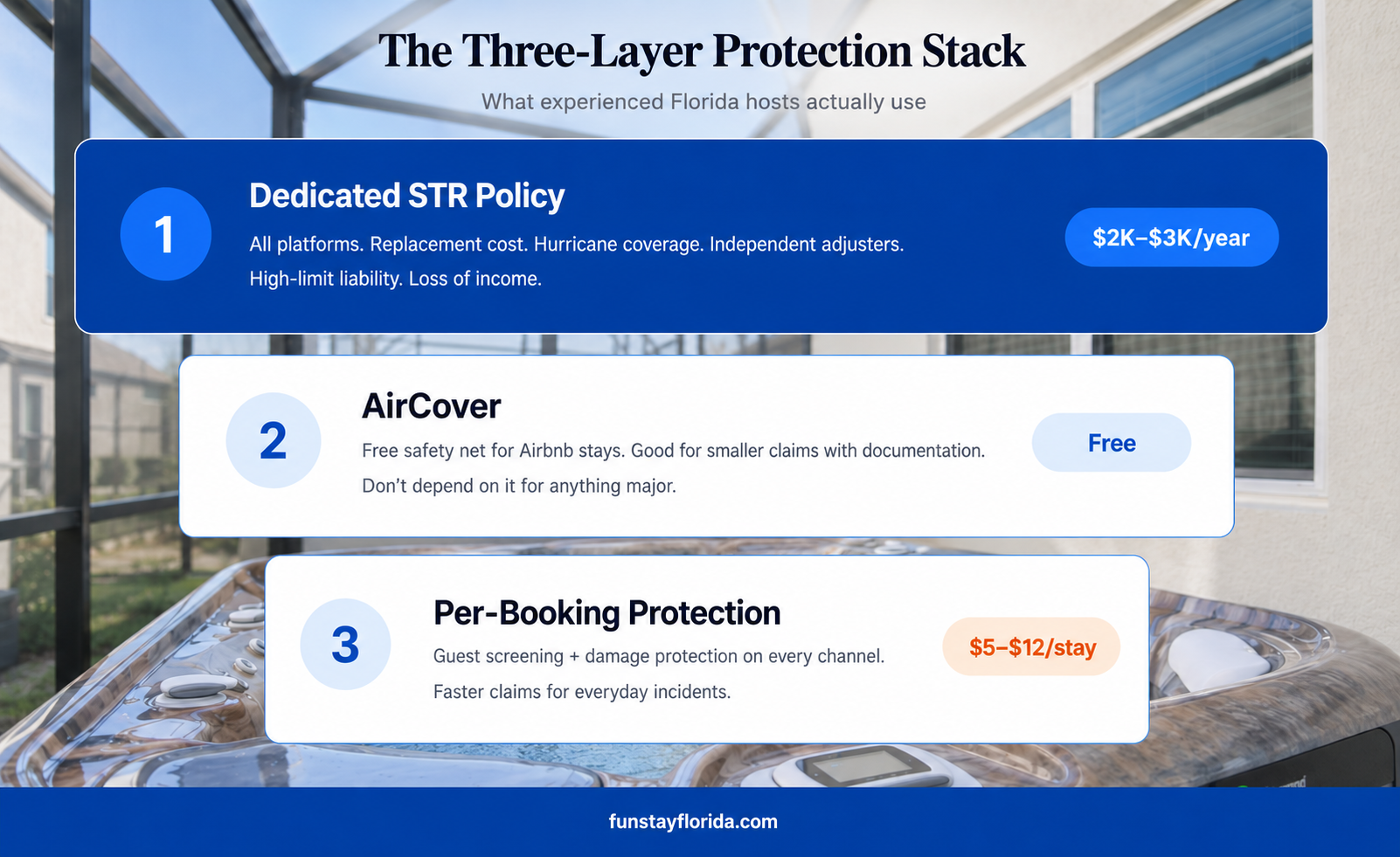

The Three-Layer Protection Stack

The answer to Airbnb AirCover vs insurance isn’t one or the other. Experienced Florida hosts use all three.

Layer 1: Dedicated STR policy ($2,000 to $3,000/year). Catastrophic loss, high-limit liability, all platforms, replacement cost, hurricane coverage, and independent adjusters.

Layer 2: AirCover (free). Keep it as a no-cost safety net for Airbnb stays. Good for smaller claims with strong documentation. Don’t depend on it for anything major.

Layer 3: Per-booking protection ($5 to $12/booking). Guest screening plus damage protection on every channel. Faster claims resolution for everyday incidents.

What FunStay Florida Does for Our Owners

Truvi damage protection on every booking. $50,000 per incident, every platform: Airbnb, VRBO, Booking.com, Expedia, Google Vacation Rentals, and our direct booking site FunStay Homes.

Trusted insurance provider connections. We make sure your short term rental insurance Florida policy meets Orlando’s licensing requirements, your vacation rental pool liability is covered, and there are no gaps between platforms.

100+ properties under management. 4.81-star average. 77% occupancy. Understanding Airbnb AirCover vs insurance is the first step. Setting up the right Florida vacation rental liability protection is what actually makes the difference.

If you’re running a vacation rental in Florida, your insurance stack is either protecting you or it’s a problem waiting to happen.

Protect Your Florida Rental the Right Way

Insurance, guest screening, and damage protection on every platform. No gaps.

Frequently Asked Questions

{kind=link}