Let’s skip the legal jargon and talk numbers. Setting up an LLC for a vacation rental in Florida costs about $375. A single slip-and-fall lawsuit in Florida settles for $75,000 to $175,000 on average. Severe cases? A Broward County jury returned a $7.5 million verdict in 2024 for a spinal injury on a commercial property.

If you own a short-term rental in Orlando, Kissimmee, or Davenport, you’re running a hospitality business whether you think of it that way or not. Strangers sleep in your home, swim in your pool, and cook in your kitchen. An LLC for your Florida vacation rental puts a legal wall between that business risk and your personal savings, your home, and your retirement accounts.

Here’s exactly what an LLC does for you, what it costs, and what to watch out for.

What an LLC Actually Does (In Plain English)

An LLC (Limited Liability Company) creates a separate legal entity that owns your rental property. If a guest gets hurt and files a lawsuit, they sue the LLC. Not you personally. The LLC’s assets are on the line (the property itself, its rental income, its insurance). Your personal bank account, your primary home, and your other properties are protected.

This protection works both ways. If you get sued personally for something unrelated to the rental, your creditors can’t easily reach the LLC’s property either.

Without an LLC

A lawsuit against your vacation rental exposes everything you own. Your savings, your car, your home, your other properties. One bad incident can contaminate your entire financial life.

Vacation rentals carry more liability than long-term rentals. Your guests are unfamiliar with the property. They’re more likely to use the pool, the hot tub, and the game room. They often bring kids and large groups. And in Florida specifically, pool liability is a serious concern. Florida recorded 112 child drownings in 2025, the highest in the nation. 64% of those happened in pools, hot tubs, or spas.

What It Costs to Set Up a Florida LLC

Less than you think. Florida is one of the most affordable states for LLC formation. Here’s the full breakdown from Sunbiz.org (Florida Division of Corporations):

| Item | Cost |

|---|---|

| Articles of Organization filing | $100 |

| Registered Agent designation | $25 |

| Annual Report (due Jan 1 to May 1 each year) | $138.75/year |

| Registered Agent service (if not self-serving) | $100–150/year |

| EIN from the IRS | Free |

| Operating Agreement (DIY or attorney) | $0–500 |

| Total Year One | $375–825 |

| Annual Ongoing | $240–290 |

Online filing through Sunbiz processes in 1 to 3 business days. Florida doesn’t charge a state income tax on LLC profits, and there’s no franchise tax like California’s $800 minimum. Your rental income passes through to your personal federal return on Schedule E, exactly like it would without an LLC.

One important note for out-of-state owners. You don’t need to be a Florida resident to form a domestic Florida LLC. You just need a registered agent with a physical Florida address. But a Florida LLC does not eliminate state income tax obligations in your home state on Florida-source rental income.

Timing matters:

Decide whether to file your DBPR vacation rental license under your personal name or your LLC before you apply. This decision is hard to change later and affects your tax reporting and liability structure going forward.

The New Florida Series LLC (Effective July 1, 2026)

This is the part that changes the math for anyone with more than one property.

Florida Senate Bill 316 was signed by Governor DeSantis on June 20, 2025, and takes effect July 1, 2026. It passed the Senate 35-1 and the House 115-0, with overwhelming bipartisan support.

Here’s what it does. A Protected Series LLC lets one parent LLC create multiple internal divisions called “protected series.” Each series holds a separate property with its own assets, liabilities, members, and bank accounts. The key benefit is horizontal liability protection: the debts and obligations of one series cannot be enforced against the assets of another series or the parent LLC.

How This Works for Vacation Rental Owners

Say you own properties in Solara Resort, ChampionsGate, and Reunion Resort. Before this law, you needed three separate LLCs ($125 filing each, three annual reports at $138.75, three registered agent fees, three sets of tax filings). That’s roughly $1,700 in year one and $1,200+ every year after.

With a Series LLC, you file one parent LLC and create three protected series. One annual report. One registered agent. If a guest sues over an injury at the Solara property, they can only go after that series’ assets. The ChampionsGate and Reunion properties are legally walled off.

| Item | Series LLC (3 properties) | 3 Separate LLCs |

|---|---|---|

| Formation | 1 parent ($125) + 3 series | 3 x $125 = $375 |

| Annual Reports | 1 x $138.75/yr | 3 x $138.75 = $416.25/yr |

| Registered Agent | ~$125/yr | 3 x $125 = $375/yr |

| Annual Savings | ~$630/year saved with Series LLC |

Fair warning

This law is brand new. There is zero Florida case law testing the liability shield yet. Many banks don’t open accounts for individual series. Many insurance carriers don’t understand series LLCs and may struggle to allocate coverage properly. And the liability shield only holds if you maintain strict, separate records for each series. If your bookkeeping gets sloppy, a court can pierce the shield. Talk to an attorney who specifically understands this new statute before setting one up.

The Mortgage Problem (and How to Solve It)

This is the part that worries most owners, and it’s a real concern. Transferring a property from your personal name to an LLC technically triggers the due-on-sale clause in your mortgage. The Garn-St. Germain Act protects transfers to trusts, but it does not protect LLC transfers.

In practice, lenders rarely call the loan on a property that’s current. But they legally can. Here are the three paths owners actually use:

Option 1: Get written lender consent. The safest approach. Call your lender, explain the transfer, and get it in writing. Not always granted, but many lenders will agree if payments are current.

Option 2: Use the Fannie Mae allowance. Fannie Mae permits post-closing transfers to an LLC if the original borrower maintains majority control of the LLC. This applies to loans purchased or securitized after June 1, 2016.

Option 3: Refinance into a DSCR loan under the LLC. This is the cleanest fix. DSCR (Debt Service Coverage Ratio) loans qualify based on the property’s income, not your personal income. They fully support LLC ownership. Rates run 6.875% to 7.5% for strong profiles (FICO 740+, DSCR 1.25+) as of June 2026. The rate gap versus conventional investment loans has narrowed to about half a point.

Title insurance note

Your existing title insurance policy names you personally, not the LLC. Transferring ownership may void it. Before you transfer, contact your title company and request a 107.9 endorsement ($100–150) to add the LLC as an insured party.

Insurance: The LLC’s Partner, Not Its Replacement

An LLC without proper insurance is like a seatbelt without airbags. It helps, but it’s not the full picture.

Here’s the issue. If the LLC owns the property but your insurance is still in your personal name, claims can be denied. The ownership change usually means switching from a personal homeowner’s policy to a commercial short-term rental policy.

In the Orlando, Kissimmee, and Davenport market, short-term rental insurance runs $2,000 to $4,000 per year for inland properties. Properties with pools should carry $1M to $2M in primary liability plus a $1M to $5M umbrella policy.

What About Airbnb AirCover?

AirCover is not a substitute for real insurance or a real business structure. Here’s why:

Host Damage Protection covers up to $3M, but it’s not insurance. Airbnb pays at their own discretion, and only at depreciated value. Not replacement cost. Host Liability Insurance covers up to $1M per stay and is real insurance through Zurich. But you are not a named insured. You have no direct policy rights.

Key exclusions: mold, assault, communicable disease, pollution, punitive damages. There’s a 14-day claim filing deadline with no exceptions. And according to Hostfully, 78% of hosts without dedicated STR coverage have had claims denied.

The Tax Angle Most Owners Miss

An LLC doesn’t change your tax rate. But it does change how organized and protected you are, and it makes it easier to take advantage of deductions you might be leaving on the table.

The big 2026 development: the Big Beautiful Bill restored 100% first-year bonus depreciation permanently for property acquired and placed in service after January 19, 2025. That means if you buy furniture, appliances, or eligible improvements for your rental, you can write off the full cost in year one.

Pair that with a cost segregation study ($2,000 to $5,000 for a desktop version), and you can reclassify 20% to 40% of your building’s depreciable basis from 27.5 years into 5, 7, or 15-year categories. On a $500,000 property with roughly $400,000 in depreciable basis, that’s $100,000 to $150,000 in accelerated first-year deductions. The ROI on a cost segregation study is typically 5x to 10x the cost.

And there’s the STR tax loophole. Rentals with average stays under 7 days aren’t classified as “rental activities” under IRC Section 469. If you materially participate (100+ hours per year and more than any other individual), your losses become non-passive and can offset your W-2 income. You don’t need to qualify as a Real Estate Professional for this. A tax CPA who specializes in short-term rentals can walk you through whether this applies to your situation.

One more thing. Florida charges sales tax plus tourist development tax on all short-term stays. In Orange County (Orlando), the total is 12.5%. In Osceola County (Kissimmee), it’s 13.5%. In Polk County (Davenport), it’s about 11%. A professional property manager handles the collection and remittance of these taxes for you.

FunStay Florida Handles the Complexity

We manage licensing, tax compliance, insurance coordination, and vendor relationships for 100+ Orlando-area vacation rentals. You focus on the returns. We handle the rest.

When You Don’t Need an LLC

To be fair, an LLC is not mandatory. If all of these apply to you, you might be fine without one:

- You own a single property with minimal personal assets at risk

- You carry strong liability insurance ($1M+ with an umbrella policy)

- The property has no pool, hot tub, or other high-risk amenities

- You have no other investment properties that could be exposed

Even then, most attorneys in the Florida vacation rental space recommend an LLC. At $240 per year in ongoing costs, the liability shield is cheap peace of mind.

When You Absolutely Need One

If any of these describe your situation, an LLC for your Florida vacation rental isn’t optional. It’s overdue:

- You own multiple properties (the new Series LLC was built for you)

- Your property has a pool or hot tub (Florida leads the nation in child drownings)

- You live out of state and can’t personally oversee the property

- You have significant personal assets worth protecting

- You’re expanding your vacation rental portfolio and want to scale professionally

The question isn’t really whether you need an LLC. The question is whether you can afford not to have one when a guest slips on a wet pool deck or a hot tub malfunctions during a family reunion.

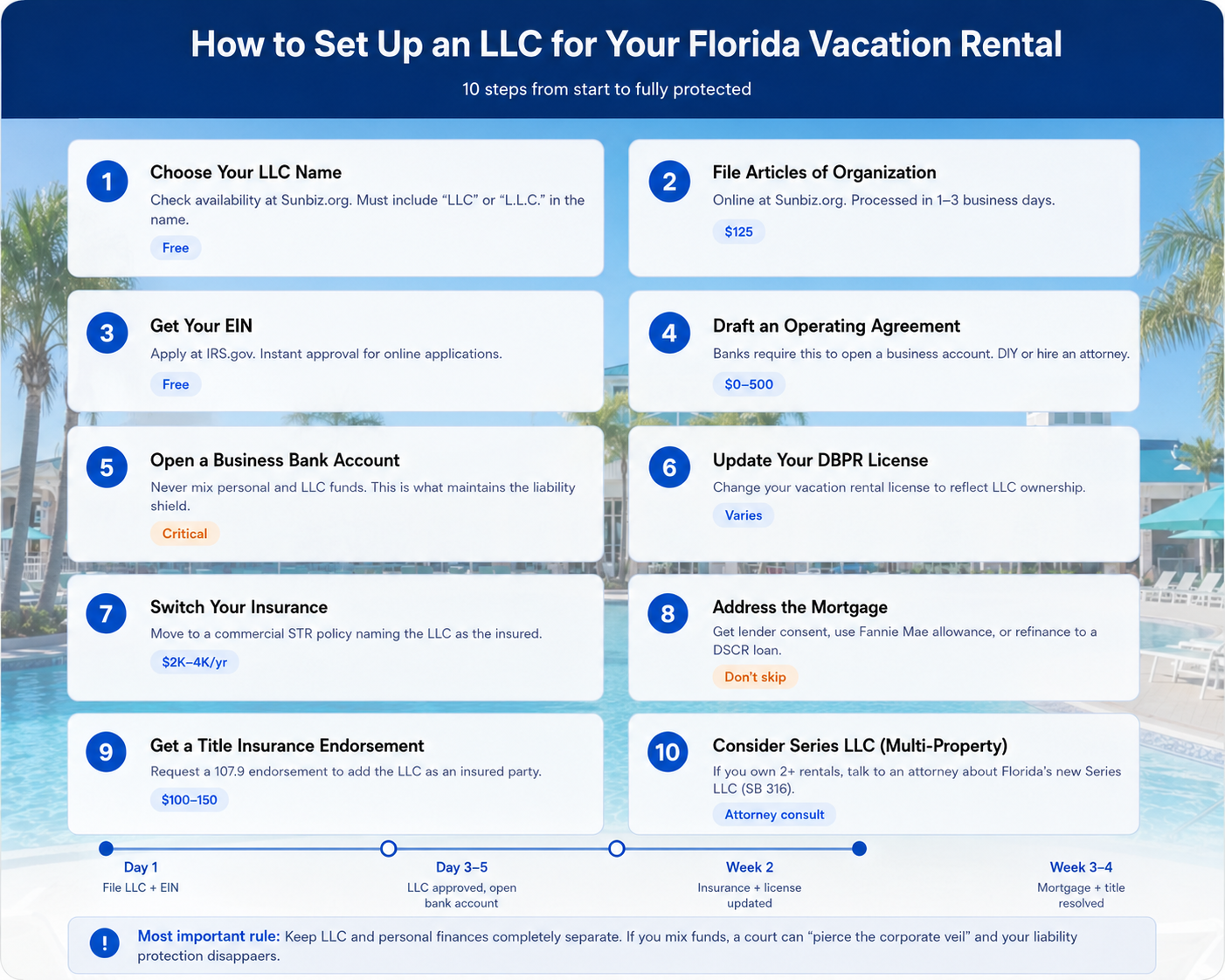

How to Set It Up (Step by Step)

- Choose your LLC name and check availability at Sunbiz.org

- File Articles of Organization online ($125, approved in 1–3 business days)

- Get your EIN from the IRS (free, instant at irs.gov)

- Draft an operating agreement (banks require this to open a business account)

- Open a dedicated business bank account (never mix personal and LLC funds)

- Update your DBPR vacation rental license to reflect LLC ownership

- Switch your insurance to a commercial STR policy naming the LLC

- Address the mortgage (lender consent, Fannie Mae allowance, or DSCR refinance)

- Get a title insurance endorsement (107.9 endorsement, $100–150)

- If you own multiple properties, talk to an attorney about the new Series LLC structure

Disclaimer

This article is educational, not legal or tax advice. Every owner’s situation is different. Work with a Florida real estate attorney and a CPA who specializes in short-term rentals before making structural decisions about your property.

Frequently Asked Questions

{kind=link}